- Knight Frank: Africa’s Prime Office Occupancy Surpasses 80% as Logistics Assets Emerge as Top Performers;

- Key Prime Office Occupancies in Selected Markets (Q1 2026):

Kenya – 80.3%

South Africa – 93%

Uganda – 84%

Africa’s real estate market is shifting from a period of general recovery into a more selective, quality-driven growth cycle.

This transition is being driven by investors and occupiers recalibrating their strategies in response to evolving macroeconomic conditions, changing occupier preferences, and structural supply imbalances across key markets, according to Knight Frank’s flagship Africa Report 2026/27.

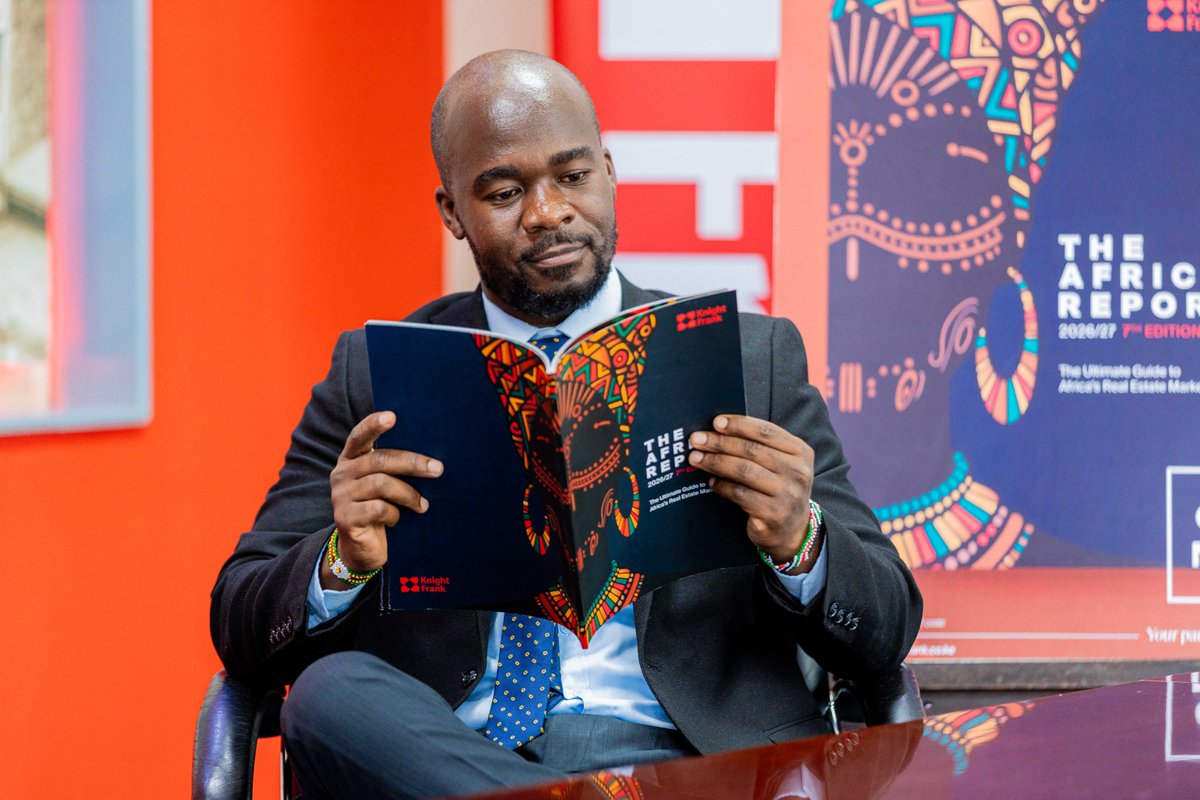

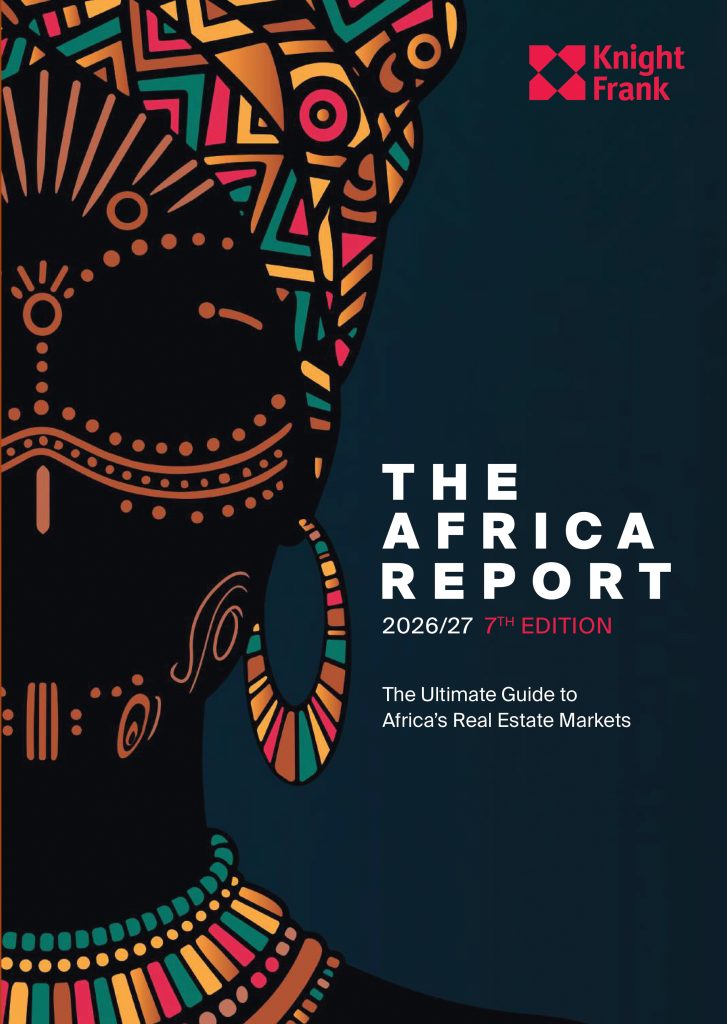

The report, officially launched at the 13th annual East Africa Property Investment (EAPI) Summit held at the Radisson Blu Hotel in Nairobi, consolidates data from 20 African markets and underscores a continent-wide convergence around four defining themes:a pronounced “flight to quality” in office markets, the rise of convenience-driven retail, sustained albeit uneven residential demand, and the continued outperformance of the industrial and logistics sectors.

The report, officially launched at the 13th annual East Africa Property Investment (EAPI) Summit held at the Radisson Blu Hotel in Nairobi, consolidates data from 20 African markets and underscores a continent-wide convergence around four defining themes:a pronounced “flight to quality” in office markets, the rise of convenience-driven retail, sustained albeit uneven residential demand, and the continued outperformance of the industrial and logistics sectors.

These findings align closely with the conference theme, “Re-newed Momentum,” which reflects a market entering a new phase of growth and consolidation.

The 2026 EAPI Summit signals the onset of a renewed investment cycle, where both international and domestic institutional capital are increasingly backing proven, resilient, and scalable operators.

The 2026 EAPI Summit signals the onset of a renewed investment cycle, where both international and domestic institutional capital are increasingly backing proven, resilient, and scalable operators.

Flight to quality dominates the office market

According to Knight Frank, across Africa’s major commercial hubs, from Cairo and Lagos to Nairobi and Johannesburg, the office sector is being redefined by a decisive shift towards Grade A, ESG-compliant buildings.

Boniface Abudho, Research Analyst- Knight Frank Africa, explains, “The continent-wide “flight to quality” is translating into tightening vacancies in prime assets, even as secondary stock faces mounting pressure. In Nairobi, for instance, prime office occupancy has risen to 80.3%, while in South Africa, vacancies in prime districts have compressed to as low as 6.8%, and even lower in top-tier precincts.

Boniface Abudho, Research Analyst- Knight Frank Africa, explains, “The continent-wide “flight to quality” is translating into tightening vacancies in prime assets, even as secondary stock faces mounting pressure. In Nairobi, for instance, prime office occupancy has risen to 80.3%, while in South Africa, vacancies in prime districts have compressed to as low as 6.8%, and even lower in top-tier precincts.

“Across sectors, a clear pattern is emerging: quality is outperforming quantity.Whether in prime office assets,convenience-led retail, high- end residential, or logistics-driven industrial developments, success is increasingly defined by location, specification, and alignment with structural demand drivers.”

“Across sectors, a clear pattern is emerging: quality is outperforming quantity.Whether in prime office assets,convenience-led retail, high- end residential, or logistics-driven industrial developments, success is increasingly defined by location, specification, and alignment with structural demand drivers.”

Desmond Namangale, Managing Director, Knight Frank Malawi, added, “The Malawi office market is entering a period of adjustment,with a clear differentiation emerging between modern assets and ageing stock. While parts of Lilongwe are experiencing occupancy pressure, well-located Grade A buildings with strong operational resilience continue to attract demand.”

The report also indicates that, by contrast, ageing Grade B stock across markets such as Lagos, Kampala, and Bulawayo continues to record elevated vacancy levels, in some cases exceeding 40% (Bulawayo).

The report also indicates that, by contrast, ageing Grade B stock across markets such as Lagos, Kampala, and Bulawayo continues to record elevated vacancy levels, in some cases exceeding 40% (Bulawayo).

This is in line with the same trend previously recorded by Knight Frank, where occupiers are focused primarily on best-in-class space, given that offices today act more like showrooms, helping companies attract and retain talent as well as new business.

Knight Frank notes that the office monthly rental performance remains bifurcated across the continent.Prime office rents range from approximately US$ 10 psm in Tunisia and Zimbabwe to US$ 55 psm in Lagos, one of the highest on the continent, while markets such as Kinshasa command around US$ 35 psm due to severe supply constraints.

Knight Frank notes that the office monthly rental performance remains bifurcated across the continent.Prime office rents range from approximately US$ 10 psm in Tunisia and Zimbabwe to US$ 55 psm in Lagos, one of the highest on the continent, while markets such as Kinshasa command around US$ 35 psm due to severe supply constraints.

Furthermore, Knight Frank says that the occupier behaviour is shifting.Demand is increasingly concentrated on smaller, flexible units, typically ranging from 50 – 350 sqm, driven by SMEs and firms adapting to hybrid working models, while decentralisation towards mixed- use and suburban areas is accelerating in cities such as Harare and Lusaka.

Convenience and experiential retail on the rise According to the report, Africa’s retail landscape is undergoing a fundamental transformation, as consumer behaviour now shifts away from traditional large-format malls towards convenience-led, neighbourhood retail formats.

This is being driven by a combination of factors,including rising urbanisation, commuting cost pressures, and the rapid growth of e-commerce.

For instance, in markets such as South Africa, the rise of on-demand delivery platforms has accelerated demand for last-mile retail hubs, while in East and West Africa, neighbourhood centres are increasingly outperforming destination malls.

The Knight Frank report also identifies experiential retail as a key growth driver.Cairo’s lifestyle retail market, for example, now spans 2.6 million sqm across 82 developments, while tourism-led markets such as Morocco and Mauritius continue to benefit from rising footfall and international visitor spending.

The Knight Frank report also identifies experiential retail as a key growth driver.Cairo’s lifestyle retail market, for example, now spans 2.6 million sqm across 82 developments, while tourism-led markets such as Morocco and Mauritius continue to benefit from rising footfall and international visitor spending.

Performance across the sector remains uneven.While prime retail rents in leading centres range between US$ 20 – 65 psm, vacancy levels in some secondary malls, such as those in Cameroon, have reached circa 30%.

Meanwhile, informal retail continues to dominate across much of the continent, particularly in Sub-Saharan Africa, constraining formal retail expansion.

Marc du Toit, Head of Retail, Knight Frank Uganda, noted: “Ugandan retail is fast tracking into a formalised retail sector, from space creation to retail operations to digital payments and business processes.

The evolution has been dramatic over the past years and will gain more traction in years to come, enhancing consumer offerings and therefore boosting the propensity for higher consumer spending”.

Strong residential demand from expatriates amid affordability constraints

Strong residential demand from expatriates amid affordability constraints

The report indicates that Africa’s residential rental markets continue to demonstrate resilience, underpinned by strong demand from expatriates, high-net-worth individuals (HNWIs), and diaspora buy-to-let investors.

However, this demand is increasingly offset by persistent affordability constraints and limited access to housing finance. In Accra, for example, high-quality units command between US$ 3,000 – 4,500 per month, while in South Africa, luxury homes can rent for as much as US$ 6,500 per month in top-tier locations.

In contrast, markets such as Malawi and Zambia face structural undersupply, compounded by high mortgage rates exceeding 20% per annum in some cases.

Elsewhere, the rise of short-term rentals and holiday homes is reshaping demand patterns, with Egypt’s holiday homes market projected to generate US$ 1 billion+ in revenue by 2025, growing at approximately 7% annually.

Elsewhere, the rise of short-term rentals and holiday homes is reshaping demand patterns, with Egypt’s holiday homes market projected to generate US$ 1 billion+ in revenue by 2025, growing at approximately 7% annually.

Industrial sector remains the strongest-performing asset class;

According to Knight Frank, the industrial and logistics sector has emerged as the strongest-performing asset class across the continent, driven by the expansion of trade corridors, Special Economic Zones (SEZs), and e-commerce.

Across markets such as Kenya, Tanzania, Zambia, and Morocco, demand for modern warehousing continues to outstrip supply. Prime rents typically range between US$ 3–7 psm,while yields reach as high as 12.5% in Zambia, significantly outperforming other asset classes.

The report also notes that infrastructure development is a key catalyst.Projects such as the Standard Gauge Railway in East Africa, port expansions in Dar es Salaam and Durban,and the growth of SEZs in Nigeria and Ghana are reshaping logistics networks and driving demand for industrial space.

The report also notes that infrastructure development is a key catalyst.Projects such as the Standard Gauge Railway in East Africa, port expansions in Dar es Salaam and Durban,and the growth of SEZs in Nigeria and Ghana are reshaping logistics networks and driving demand for industrial space.

However, supply remains constrained. Much of the existing stock is low specification, with modern Grade A facilities limited, particularly in markets such as Kinshasa and Maputo.

In the West African powerhouse of Nigeria, office occupancy levels are improving, while convenience retail continues to expand.

Elsewhere, demand is growing for industrial and logistics space in SEZs due to the favourable leasing terms, including tax exemptions and improved infrastructure.

Frank Okosun,Managing Director- Knight Frank Nigeria, indicated, “Grade A office absorption is firming, industrial and logistics demand is accelerating within Special Economic Zones (SEZS), and residential dynamics is reshaping the city’s geography.

Frank Okosun,Managing Director- Knight Frank Nigeria, indicated, “Grade A office absorption is firming, industrial and logistics demand is accelerating within Special Economic Zones (SEZS), and residential dynamics is reshaping the city’s geography.

The foundations for sustained growth are being laid, but the next phase will require policy consistency and a continued focus on infrastructure to unlock the market’s full potential.”

In East Africa, Kenya is experiencing increased demand for grade A offices, while in contrast, vacancy rates for grade B offices are rising.

In the retail sector, near-universal smartphone penetration is enabling deeper integration of physical and digital strategies, with retailers now seeking locations that support last-mile delivery and click-and-collect services.In the hospitality sector, guest experiences have become increasingly important.

Mark Dunford, CEO, Knight Frank Kenya said,“Today,Kenya’s hotels and wider hospitality sector are no longer defined solely by room inventory constraints or seasonal demand cycles,but increasingly by the quality of guest experiences, the strategic positioning of assets, which is creating opportunities for long-term investment value.”

Mark Dunford, CEO, Knight Frank Kenya said,“Today,Kenya’s hotels and wider hospitality sector are no longer defined solely by room inventory constraints or seasonal demand cycles,but increasingly by the quality of guest experiences, the strategic positioning of assets, which is creating opportunities for long-term investment value.”